The News: Marvell Technology, a supplier of infrastructure semiconductor solutions, reported financial results for the first quarter of fiscal year 2023. Net revenue for the first quarter of fiscal 2023 was $1.447 billion, which exceeded the midpoint of the Company’s guidance provided on March 3, 2022. GAAP net loss for the first quarter of fiscal 2023 was $(166) million, or $(0.20) per diluted share. Non-GAAP net income for the first quarter of fiscal 2023 was $448 million, or $0.52 per diluted share. Cash flow from operations for the first quarter was $194.8 million. Read the Marvell Press Release here.

Marvell Kicks Off Fiscal 2023 on a High Note with Robust Q1 Financial Results

Analyst Take: Per our research note in March 2022 about the company’s Q4 2022 earnings report, Marvell Technology is on a continued streak of generating impressive earnings numbers. For fiscal Q1 2023, this track record continues, further validating Marvell’s market position and recent strategic deal making. The company’s Q1 ended on April 30. 2022. Here are the latest financial highlights:

- Q1 2023 fiscal net revenue was $1.45 billion, up 74 percent year-on-year, which exceeded the company’s guidance provided on March 3, 2022.

- Q1 2023 fiscal GAAP net loss for the first quarter of fiscal 2023 was $(166) million, or $(0.20) per diluted share.

- Q1 2023 fiscal non-GAAP net income was $448 million, or $0.52 per diluted share. Cash flow from operations for the first quarter was $194.8 million.

Marvell’s Q1 numbers beat across the board, including a record first quarter of $1.45 billion. This is a remarkable financial performance overall, and it shows how the company is advancing its strategic mission to diversify and grow its data infrastructure business and expertise to meet the evolving and growing needs of organizations across the digital ecosystem. For instance, Marvell President and CEO, Matt Murphy, emphasized that higher-than-forecasted results from the datacenter end market fueled revenue exceeding the midpoint of guidance.

Also check out: Hear more about Marvell’s strategic bets at the 2022 Six Five Summit. Sign up now.

With its core business in semiconductors and increasingly software, Marvell has fully pivoted to capitalize on the market opportunity beyond its previous consumer-focused specialization. This has continued to prove itself a critical transformation as it has been key to the company’s sustained earnings growth and sturdy diversification into key market segments.

The strong results including high double-digit and triple-digit growth in numerous areas is indicative of both a well-run strategy by Marvell, and also a broader microenvironment that is driving enterprise tech spend in deflationary technologies like AI, 5G, and Cloud. We see Marvell now as a major player across the semiconductor space that exercises considerable ecosystem influence and proven adept at uniquely capitalizing on secular growth drivers across the data infrastructure, cloud, 5G, and auto market segments to help power long-term growth.

We also find noteworthy Marvell’s M&A acumen as the company continues to obtain technology assets and expertise that swiftly augments its portfolio and bolsters its overall competitiveness. The May 2022 acquisition of Tanzanite Silicon through an all-cash transaction, which is designated to close by end of fiscal Q2 2023, can enable Marvell to broaden its addressable market and channel relations across the cloud-optimized silicon market segment.

We see this acquisition as an intelligent tuck in to the existing portfolio that will enable Marvell to lock in Compute Express Link (CXL) benefits such as extending the infrastructure agility needed to immediately allocate resources aligned to workload requirements which can produce improvement in use optimization as well as reduced total cost of ownership. Now Marvell can use CXL technology to power the built-out of fully disaggregated architectures as data center environments demand more higher speed interconnectivity coupled with optimized compute, networking, memory, security, and storage silicon fabrics and chipset solutions.

Specifically, Marvell sees the potential to embed CXL IP in a broad range of its datacenter products, including ASICs, custom compute engines, DPUs, electro optics, retimers, SmartNICs, and SSD controllers.

The Tanzanite deal follows on Marvell’s string of acquisitions that included Innovium for $1.1 billion in August 2021 and the completion of the Inphi acquisition for $10 billion in April 2021. We have been swayed by the size and strategic fit of its recent deals. Naturally, acquisitions come with risk, but these deals, together with Marvell’s existing portfolio and expertise, are setting it on a path for continued and sustained growth in a business marketplace that is generating heavy demand for these technologies and accompanying integration services.

Marvell’s Q1 2023 Performance by Market

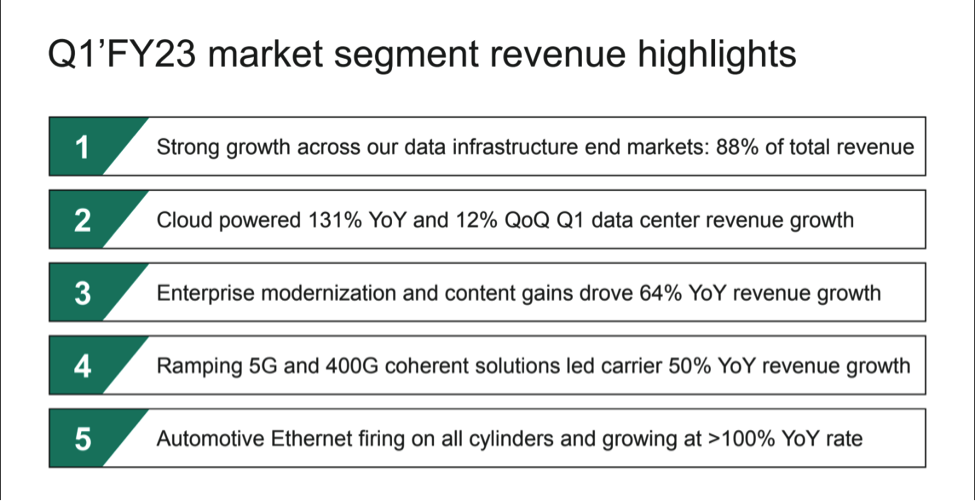

The strong results in Q1 2023 revenue figures for Marvell appear across the company’s departments as well. Revenue for Q1 in Data Center sales was $640.5 million, up 131 percent from $277.1 million in the same quarter one year ago. Revenue for Q1 in Carrier Infrastructure was $252 million, up 50 percent from $167.6 million one year ago. Revenue for Q1 in Enterprise Networking was even hotter, with $286.6 million in sales, up 64 percent from $174.8 million one year ago. Automotive and Industrial Q1 revenue totaled $89.3 million, up 94 percent from $46.1 million one year ago. And in Consumer Sales revenue for Q1, the company posted $178.5 million, up 7 percent from $166.7 million in the same quarter one year ago.

Here is a look at the breakdown of market segment highlights:

Those revenue figures also demonstrated shifts in Marvell’s revenue by end market segment. For Q1 2023, the Data Center end market segment brought in 44 percent of the company’s overall revenue, up from 33 percent a year ago, while the Carrier Infrastructure end market segment brought in 18 percent of the total revenue, down from 20 percent one year ago. The Enterprise Networking end market segment brought in 20 percent of the Q1 revenue, down from 21 percent a year ago. The Automotive/Industrial end market segment brought in 6 percent of total revenue, same as the 6 percent in the same quarter in 2021, while the Consumer end market segment brought in 12 percent in Q1 down from 20 percent a year ago.

Since Marvell changed its reporting and provided more insights into markets, it has also helped the market and analysts better understand the company’s trajectory. The participation in secular trends including 5G, Automotive, Datacenter, Cloud, and Edge, are all material growth opportunities, which is reflected in its recent growth. While tech names have pulled back from all-time highs, Marvell’s performance has decoupled from the price action. And the demand and results indicate longer term promise for the company.

Marvell’s FY2023 Outlook

Marvell is making it clear that it is not resting on its laurels. The company announced it has shipped more than 100,000 400G Coherent Digital Signal Processors (CDSPs), developed to enable open and standards-based pluggable solutions for cloud and carrier networks worldwide. Marvell’s CDSP portfolio includes Canopus, breakthrough 7nm CDSP enabling 400G ZR/ZR+, metro and long haul pluggable optical modules, and the Marvell® Deneb, an ultra-low power, multi-mode 400G DSP for OpenZR+ and OpenROADM.

From our perspective, Marvell adroitly used OFC 2022 to promote the expansion of its cloud-optimized portfolio. In particular, the new Alaska A DSPs broadens Marvell’s lineup of high-speed transceivers, including line card retimers, gearboxes, and MACsec PHYs supporting up to 800G rates, as well as active optical cable (AOC) interconnect solutions. The new offering targets the unique demands of each cloud customer such as architectures, speeds, security, and distances.

As we see it, FY2023 should be another good year for Marvell, with continuing growth and steady leadership as it bolsters its market presence and mind share in the data infrastructure tech market.

Marvell has released estimates for its Q2 FY2023 outlook, calling for net revenue of about $1.515 billion and a non-GAAP gross margin of about 65 percent to 65.5 percent. The non-GAAP expected diluted earnings per share is expected to be 56 cents per share. A sound quarter with continued positive momentum, hard not to expect more of the same in the company’s next quarter, which will report in September.

Disclosure: Futurum Research is a research and advisory firm that engages or has engaged in research, analysis, and advisory services with many technology companies, including those mentioned in this article. The author does not hold any equity positions with any company mentioned in this article.

Analysis and opinions expressed herein are specific to the analyst individually and data and other information that might have been provided for validation, not those of Futurum Research as a whole.

Other insights from Futurum Research:

Marvell Injects New CXL Technology into Cloud-Optimized CXL Portfolio with Tanzanite Acquisition

OFC 2022: Marvell Debuts CPO Platform to Spur Open Switch and Optics Integration

OFC 2022: Marvell Adds Unique Touch to New Cloud-Optimized 400G/800G PAM4 DSPs

Image Credit: Marvell

The original version of this article was first published on Futurum Research.

Daniel Newman is the Principal Analyst of Futurum Research and the CEO of Broadsuite Media Group. Living his life at the intersection of people and technology, Daniel works with the world’s largest technology brands exploring Digital Transformation and how it is influencing the enterprise. From Big Data to IoT to Cloud Computing, Newman makes the connections between business, people and tech that are required for companies to benefit most from their technology projects, which leads to his ideas regularly being cited in CIO.Com, CIO Review and hundreds of other sites across the world. A 5x Best Selling Author including his most recent “Building Dragons: Digital Transformation in the Experience Economy,” Daniel is also a Forbes, Entrepreneur and Huffington Post Contributor. MBA and Graduate Adjunct Professor, Daniel Newman is a Chicago Native and his speaking takes him around the world each year as he shares his vision of the role technology will play in our future.

Ron is an experienced research expert and analyst, with over 20 years of experience in the digital and IT transformation markets. He is a recognized authority at tracking the evolution of and identifying the key disruptive trends within the service enablement ecosystem, including software and services, infrastructure, 5G/IoT, AI/analytics, security, cloud computing, revenue management, and regulatory issues.